Amortization schedule templates play an important role in loan management and financial planning. These templates provide a complete breakdown of loan payments over a specific period of time. They show how each payment reduces the loan balance and how much money goes toward interest charges. People commonly use these templates for mortgages, car loans, student loans, and personal loans. A well-designed amortization schedule helps borrowers understand the structure of their loans in a simple and organized way.

Many individuals struggle to calculate monthly payments and remaining balances manually. Amortization schedule templates solve this problem by arranging all payment details in a clear table format. Users can quickly check payment dates, installment amounts, interest costs, and outstanding balances. Most templates also allow users to enter loan amounts, interest rates, and repayment periods to generate automatic calculations. This feature saves time and reduces errors in financial calculations.

Amortization Schedule Templates

Amortization schedule templates help borrowers manage their finances more effectively. They provide a clear picture of how loans work from the first payment to the final installment. Borrowers can see how interest decreases over time while the principal payment increases gradually. This understanding helps people make better financial decisions and avoid confusion about loan repayment terms. These templates also support budgeting and future financial planning. Users can estimate monthly expenses and prepare their budgets according to loan obligations. Businesses use amortization schedules to maintain accurate financial records and monitor debt repayments. Financial institutions also rely on these schedules to explain loan structures to customers and maintain transparency in lending practices.

Amortization schedule templates help users compare different loan options before making commitments. People can analyze different interest rates, repayment periods, and payment amounts to choose the most suitable loan. This comparison process helps borrowers reduce financial risks and select affordable repayment plans. In addition, borrowers can use these templates to plan extra payments and calculate how early repayments reduce loan costs and repayment time.

Accurate recordkeeping represents another major benefit of amortization schedule templates. These templates store detailed payment information in one place and help users monitor payment history easily. Borrowers can track remaining balances and ensure timely payments throughout the loan term. Organized records also help during tax preparation, financial audits, and communication with lenders.

An Amortization Schedule is a table that provides a detailed breakdown of each payment for an amortizing loan throughout its lifespan. An amortizing loan involves repayment of a loan at regular intervals whereby the initial amount borrowed decreases gradually until it is paid off fully in the end.

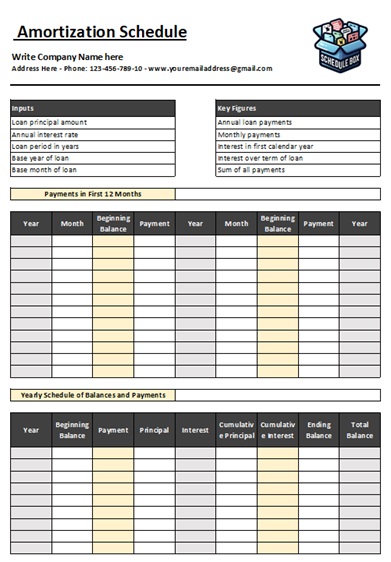

Amortization Schedule Template – Cumulative Interest

File Size: 38 KB

Amortization Schedule’s Elements

Payment Date

The payment date shows the exact day on which the borrower must make each loan payment. This section helps borrowers stay organized and avoid late payment charges. Most lenders set monthly payment dates, but some loans may require weekly, biweekly, or quarterly payments. Borrowers can use the payment date column to track upcoming installments and prepare their finances in advance. A clear payment schedule also helps people maintain a good credit history because timely payments improve financial reliability. A home loan may require payments on the first day of every month for twenty or thirty years. The amortization schedule lists every payment date from the beginning of the loan until the final installment. This organized timeline helps borrowers understand the full repayment period and monitor their financial commitments more effectively.

Payment Amount

The payment amount represents the total sum that the borrower pays during each installment period. This amount usually includes both principal and interest charges. Most fixed-rate loans maintain the same payment amount throughout the loan term, while variable-rate loans may change depending on interest rate fluctuations. Borrowers use this section to estimate monthly expenses and manage household or business budgets more efficiently.

A consistent payment amount helps borrowers plan their finances without confusion. For example, if a borrower takes a loan of $20,000 with a five-year repayment term, the amortization schedule may show a monthly payment of around $400. The borrower can then prepare for this recurring expense every month and avoid financial stress.

Principal Amount

The principal amount refers to the portion of each payment that reduces the original loan balance. At the beginning of the loan term, a smaller part of the payment goes toward the principal because interest charges remain higher. As the borrower continues making payments, the principal portion gradually increases while the interest portion decreases. This section helps borrowers understand how quickly they reduce their debt over time. For example, during the early years of a mortgage loan, only a small percentage of the monthly payment lowers the actual loan balance. However, after several years, a larger share of each payment contributes directly to reducing the remaining debt. Borrowers can monitor their financial progress by checking the principal amount in each installment.

Interest Amount

The interest amount shows the cost of borrowing money from the lender. Lenders calculate this amount based on the remaining loan balance and the interest rate. During the first stage of repayment, borrowers usually pay higher interest charges because the outstanding loan balance remains large. As the balance decreases, the interest amount also becomes smaller. This section helps borrowers understand the true cost of the loan. Many people focus only on monthly payments and ignore the total interest expense. An amortization schedule clearly explains how much money goes toward interest during every payment period. For example, a borrower with a long-term mortgage may pay thousands of dollars in interest over the life of the loan. This information encourages borrowers to make extra payments whenever possible to reduce overall interest costs.

Total Interest Paid to Date

The total interest paid to date section displays the cumulative amount of interest that the borrower has paid since the start of the loan. This running total helps borrowers measure the long-term cost of borrowing. It also allows borrowers to evaluate whether they should refinance the loan or make additional payments to lower future interest expenses. After five years of regular payments on a car loan or mortgage, a borrower may notice that a large amount of money has gone toward interest instead of principal reduction. This realization often motivates borrowers to increase monthly payments or shorten the repayment period. The cumulative interest section provides a clear financial picture and helps people make smarter financial decisions.

Remaining Balance

The remaining balance shows the unpaid portion of the loan after each payment. This section helps borrowers track how much debt still remains. After every installment, the schedule updates the remaining balance by subtracting the principal portion of the payment from the previous balance. Borrowers often use this section to monitor repayment progress and estimate the time required to become debt-free. For example, someone with a student loan can review the remaining balance each month to see how quickly the loan decreases. Businesses also use this information to manage liabilities and maintain accurate financial records. A declining balance gives borrowers confidence and motivates them to continue making regular payments.

Use of Amortization Schedules in Real Life

People commonly use amortization schedules for mortgages, car loans, personal loans, and business financing. These schedules provide a complete financial overview of the loan repayment process. Borrowers can clearly see how each payment affects the outstanding balance and total interest cost over time. Financial institutions also use amortization schedules to explain repayment structures to customers and maintain transparency in lending practices.

An amortization schedule also helps borrowers compare loan options before making financial decisions. People can analyze different repayment periods, monthly payment amounts, and interest rates to choose the most affordable option. Borrowers who plan early repayments can use the schedule to calculate how much money they can save on interest charges. This detailed financial information supports better money management and long-term financial stability.

Types of Amortization Schedules

Amortization schedules can vary based on the type of loan, the structure of payments, and specific terms agreed upon by the lender and borrower. Here are some common types of amortization schedules:

Standard Amortization Schedule:

Fixed-Rate Amortization: The most common type where the interest rate remains constant throughout the life of the loan. Payments are equally distributed over the term, with early payments consisting mostly of interest and later payments primarily reducing the principal.

Adjustable-Rate Amortization Schedule:

Adjustable-Rate Mortgage (ARM): This schedule is used for loans with interest rates that can change over time. The schedule will adjust as the interest rate changes, affecting the amount of each payment and its division between interest and principal.

Balloon Payment Amortization Schedule:

Balloon Loan: This involves regular payments calculated as if the loan will be paid over a specific period, but a final “balloon” payment— a much larger payment — is due at the end of a shorter fixed period.

Interest-Only Amortization Schedule:

Interest-Only Loan: For a certain period, the borrower pays only the interest on the principal. After this period, the schedule reverts to standard amortization where payments include both principal and interest.

Negative Amortization Schedule:

Negative Amortization Loan: This schedule allows for payments that are less than the interest charged over a period, causing the loan balance to increase rather than decrease.

Graduated Payment Amortization Schedule:

Graduated Payment Mortgage (GPM): Payments start lower and gradually increase. The schedule reflects this change, typically designed to match increases in a borrower’s income.

Custom Amortization Schedule:

Custom or Flexible Payments: Some loans allow for customized payment plans, such as varying the payment amounts or frequencies according to the borrower’s cash flow.

There are a number of financial needs and situations that can be handled by different amortization schedules, each of which offers its own ways of assisting the debtors to control their repayment given their economic condition and future expectations.

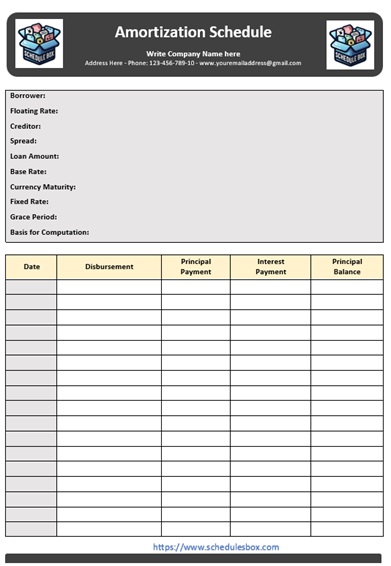

Professional Amortization Schedule Template

File Size: 104 KB

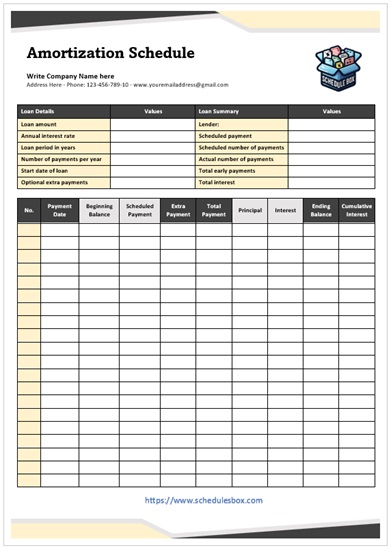

Amortization Schedule Template – Table View

File Size: 118 KB

Benefits of using our Amortization Schedule Templates

There are numerous advantages of using ready-made amortization schedule templates, particularly when it comes to individuals and business owners who want to handle their loans in an effective manner but are not required to make complex computations afresh. Here are some key advantages:

Time Savings

Amortization schedule templates save a lot of time for borrowers, business owners, and financial managers. Many people do not understand complex financial calculations, and manual calculations often create confusion. A template removes this difficulty by automatically organizing all loan details in a clear format. Users only need to enter basic information such as the loan amount, interest rate, repayment period, and start date. The template then calculates monthly payments, interest charges, principal amounts, and remaining balances within seconds. This feature becomes especially useful for people who manage multiple loans at the same time. Instead of spending hours creating tables and formulas manually, users can quickly generate complete schedules with accurate results. The time-saving advantage also allows borrowers to focus on financial planning and budgeting rather than complicated calculations.

Accuracy

Amortization schedule templates improve accuracy in loan calculations and financial records. Manual calculations often lead to mathematical errors, especially when loans involve long repayment periods or changing interest rates. Even small mistakes can create confusion about payment amounts, balances, or total interest costs. Templates reduce these risks because they use built-in formulas to perform calculations automatically.

Accurate calculations help borrowers understand their financial obligations clearly and avoid unexpected problems. Businesses and financial institutions also depend on precise loan records to maintain proper accounting systems. A reliable amortization schedule ensures that every payment, interest charge, and balance update remains correct throughout the loan term. This accuracy supports better debt management and stronger financial decision-making.

Ease of Use

Most amortization schedule templates offer a simple and user-friendly design. People with little financial knowledge can easily use these templates without professional assistance. Users usually enter only a few details, including the loan amount, interest rate, loan term, and payment frequency. After entering this information, the template automatically generates a complete payment schedule. The template clearly divides each payment into principal and interest portions while also showing the remaining loan balance after every installment. This simple layout helps borrowers understand loan repayment without confusion. Many templates also use charts, tables, and organized sections that improve readability and make financial information easier to follow.

Financial Planning

Amortization schedule templates play an important role in financial planning and budgeting. These templates allow borrowers to view the entire repayment process from the first installment to the final payment. Users can see how much money goes toward interest and how much reduces the principal balance during every payment period. This information helps borrowers plan monthly budgets more effectively and prepare for future financial commitments. Business owners can also use amortization schedules to manage cash flow and monitor debt obligations. Borrowers who want to pay off loans early can analyze the schedule and calculate how extra payments reduce interest costs and shorten repayment periods. This detailed financial overview supports smarter money management and long-term financial stability.

Consistency

Standardized amortization schedule templates create consistency in loan management and financial reporting. Companies and financial institutions often manage many loans at the same time, and consistent templates help them organize all records in the same format. This consistency improves communication, recordkeeping, and financial analysis.

When all loan schedules follow the same structure, users can compare loans more easily and identify payment patterns quickly. Consistent reporting also helps businesses maintain accurate financial statements and reduce confusion during audits or financial reviews. Borrowers benefit from this organized system because it provides clear and reliable information throughout the repayment process.

Customization

Many amortization schedule templates offer customization features that allow users to adjust the schedule according to personal or business needs. Borrowers can modify payment frequency, add extra installments, change loan terms, or adjust interest calculations based on their financial goals. For example, some users prefer weekly or biweekly payments instead of monthly installments because more frequent payments can reduce total interest costs over time. Borrowers can also include additional payments to see how quickly they can reduce the remaining balance. This flexibility helps users create repayment plans that match their income, expenses, and financial priorities. Customized templates provide better control over debt management and help borrowers achieve financial goals more efficiently.

Educational Tool

Amortization schedule templates also serve as valuable educational tools for students, borrowers, and anyone learning about loans and financial management. These templates explain how loans work in a practical and visual way. Users can observe how interest charges decrease over time while principal payments gradually increase.

This learning process helps people understand important financial concepts such as interest rates, loan terms, repayment structures, and debt reduction. Students studying finance or accounting often use amortization schedules to improve their understanding of loan calculations and financial analysis. Borrowers also gain more confidence in handling personal finances because the template presents complex financial information in a simple and easy-to-understand format. Amortization schedule templates are a handy resource for anybody dealing with loans, be it an individual borrower, a money manager, or a professional in the banking sector. They provide a good mix of ease, dependability, and insight into financial responsibilities.